Two Strategies To Accumulate Wealth

If you think that your super will be sufficient to “fall back” on if all else fails in your retirement plan – this may not truly be the case. In point of fact the mean super balance for a person aged 55 – 65 is around $165,000(1) and in 2008 almost 70%(2) of the retiring population were resorting to Government Aged Pension. Clearly employer super isn’t sufficient for the current set of retirees.

One misconception is that forgetting about superannuation and concentrating on other investments ends up with enough in retirement.

We tend to find that those people who take their super seriously also succeed in the other areas of their wealth management.

Why is this, you may ask? Well it’s not because they’re amazing at choosing investments or know something others don’t, rather it’s because they become serious about the basics… Yes the basics of consistent savings, long term investment and the marvel of compounding!

There is also some great stuff we can do if you use a mortgage offset account. FIND OUT MORE

How much is enough?

To help you understand the basics, we’ll first show you ‘How much is enough?’ For a couple aged 35 years old looking to retire at age 60 on an income of $60,000 per annum, they’ll need to have superannuation savings of around $1.1 million dollars (3). Unfortunately for them the contributions from their employer won’t cut it, even at 12%. If that same couple has an annual income of $80,000 and $50,000 in superannuation already, they’re only going to reach a balance of around $800,000 (4), that’s $300,000 short of what they really need.

1. A little less in fees

2. A little extra savings

3. Putting them both together!

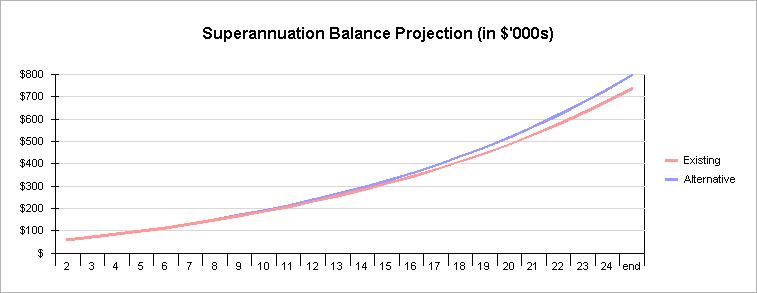

Strategy one – A little less fees in Superannuation

The power of compounding can work in both ways, in the same way that larger investment returns will increase your investment, so too will a reduction in investment fees. Look at it this way: would you rather have an investment returning 10% per annum and costing 4% in fees or an investment retuning 8% with only 1% in fees? We know which one we’d prefer.

In this strategy we look at the effect of reviewing the type of super fund you have and finding a lower cost alternative. Again using our same couple from earlier we get them to move their Super into a new fund with total fees half a percent (0.5%) cheaper per annum over the life of the investment without changing anything else.

Result: By the time they reach age 60 they would have a balance $866,524, that’s an extra $68,000, purely from saving only 0.5% in fees per annum. And this is not hard to achieve, if you find a good Superannuation Advisor they can often recommend a lower cost alternative, especially if you have multiple superannuation accounts already.

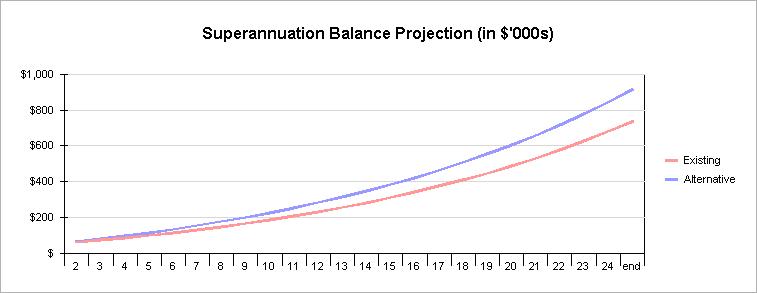

Strategy two – A little extra savings to Superannuation

Effective and consistent savings is arguably one of the most powerful habits of any successful investor. Take for example Warren Buffet, who made his first major investment at age 14 with $1,200 he saved doing a newspaper round, through adding more to his investment and then reinvesting the profits he now has a personal net worth of $47 Billion. “When you first make money, you may be tempted to spend it. Don’t. Instead, reinvest the profits”.

In this strategy we look at the effects of saving just a little extra via salary sacrifice. For a person earning $80,000 per annum an extra 5% per year is only $10.95 per day, probably less than you would spend on lunch! Using the same couple as in the last strategy they add an extra $10.95 per day to super without changing anything else.

Result: By the time they reach age 60 they would have a balance $988,000, that’s an extra $190,000!

Putting both strategies together!

Finally let’s see what happens when our couple puts strategy one and two together. An extra $4,000 per annum in salary sacrifice and a saving in fees of 0.5%.

Result: By the time they reach age 60 they would have a projected Super balance of $1.076 million. That’s an extra $278,000!!! Much closer to their goal of $60,000 per annum income in retirement.

Getting started on the basics

So there you have it, simply doing the basics consistently right will make a world of difference for your retirement planning and wealth creation and trust us; saving a little extra won’t break the bank, once you start you won’t even notice it. Applying this same set of principles across all your investments, not just superannuation then becomes easy and with that you will have even greater success.

If you are going to make one smart financial commitment this year it should be to speak to your Superannuation Advisor so that you too can make a start on these basics.

General Advice Warning: It is important for you to note that in preparing this article Cedar Wealth Financial Advisers have not taken into account any particular persons objectives, financial situation or needs. Investors should, before acting on this information, consider the appropriateness of this information having regard to their personal objectives, financial situation or needs. We recommend investors obtain financial advice specific to their situation before making any financial investment or insurance decision.

1. ABS 4102.0 – Australian Social Trends, March 2009 Pg 2.

2. Employment Arrangements, Retirement and Superannuation, Australia, April to July 2007 (Reissue)

(ABS cat. no. 6361.0).

3. This figure was derived using an annual income return of 5.5% p.a. net of fees and taxes.

4. For our projections we assumed a ‘Balanced’ total return of 8.5% p.a. net of taxes and fees and SCG

contributions of 12% p.a.