Your eyes may already be rolling in the back of your head. Not another post about super, you may say.

Have you heard of the “carry forward unused concessional super contributions” rule?

As the the end of the financial year approaches, many look for ways to reduce assessable and taxable income.

Have you fully used the concessional super contributions, including unused contributions.

This is one tax reduction strategy as concessional super contributions are a tax deduction up to their cap.

If you would like to chat to us about some options – feel free to contact us: info@cwmm.com.au

It seems like June 30 rolls around quicker every year, so why wait until the last minute to get your finances in order?

With all the disruption and special support measures of the past two years, it’s possible your finances have changed. So it’s a good idea to ensure you’re on track for the upcoming end-of-financial-year (EOFY).

Starting early is essential to make the most of opportunities on offer when it comes to your super and tax affairs.

New limits for super contributions

Annual contribution limits for super rose this financial year, so maximising your super contributions to boost your retirement savings is even more attractive.

From 1 July 2021, most people’s annual concessional contributions cap increased to $27,500 (up from $25,000). This allows you to contribute a bit extra into your super on a before-tax basis, potentially reducing your taxable income.

If you have any unused concessional contribution amounts from previous financial years and your super balance is less than $500,000, you may be able to “carry forward” these amounts to further top up.

Another strategy is to make a personal contribution for which you claim a tax deduction. These contributions count towards your $27,500 cap and were previously available only to the self-employed. To qualify, you must notify your super fund in writing of your intention to claim and receive acknowledgement.

Non-concessional super strategies

If you have some spare cash, it may also be worth taking advantage of the higher non-concessional (after-tax) contributions cap. From 1 July 2021, the general non concessional cap increased to $110,000 annually (up from $100,000).

These contributions can help if you’ve reached your concessional contributions cap, received an inheritance, or have additional personal savings you would like to put into super. If you are aged 67 or older, however, you need to meet the requirements of the work test or work test exemption.

For those under age 67 (previously age 65) at any time during 2021-22, you may be able to use a bring-forward arrangement to make a contribution of up to $330,000 (three years x $110,000).

To take advantage of the bring-forward rule, your total super balance (TSB) must be under the relevant limit on 30 June of the previous year. Depending on your TSB, your personal contribution limit may be less than $330,000, so it’s a good idea to talk to us first.

More super things to think about

If you plan to make tax-effective super contributions through a salary sacrifice arrangement, now is a good time to discuss this with your employer, as the ATO requires documentation prior to commencement.

Another option if you’re aged 65 and over and plan to sell your home is a downsizer contribution. You can contribute up to $300,000 ($600,000 for a couple) from the proceeds without meeting the work test.

And don’t forget contributing into your low-income spouse’s super account could score you a tax offset of up to $540.

Know your tax deductions

It’s also worth thinking beyond super for tax savings.

If you’ve been working from home due to COVID-19, you can use the shortcut method to claim 80 cents per hour worked for your running expenses. But make sure you can substantiate your claim.

You also need supporting documents to claim work-related expenses such as car, travel, clothing and self-education. Check whether you qualify for other common expense deductions such as tools, equipment, union fees, the cost of managing your tax affairs, charity donations and income protection premiums.

If 2016 taught us anything, it was to expect the unexpected. Britain’s vote to exit the European Union and Donald Trump’s election as the next US President surprised the pundits and markets alike. Markets generally hate surprises, yet in the closing weeks of the year so-called ‘Trump trades’ pushed shares, bond yields and the US dollar.

READ ABOUT 2016 – THE YEAR IN REVIEW

New Year is traditionally the season of fresh starts and personal resolutions. Along with diet and exercise, getting ahead financially makes it onto many wish lists year in and year out. But a brighter financial future is likely to remain a pipedream without a back-up if things don’t go to plan. READ MORE HERE ABOUT WHAT TO DO

Before you carry on reading, let me warn you that the content of this article is going to be confronting.

As a scenario – you and your business partner own the shares in your trading company. Let’s assume it is correctly structured.

However, one key element has been overlooked. There is no written and documented buy sell agreement.

Your business partner passes away and once the funeral is over, their estate has been settled and the reality has set in, that person’s spouse walks into your office and says: “Hi, I am your new business partner”.

Dumbfounded, you think: “How is that possible?”

Reading your thoughts, he | she says: “My spouse left the shares in the business to me – in the will”.

Is that really what the intention was? How are you going to manage that “new” relationship? Maybe it’s fine. But on the other hand, maybe it isn’t.

What can you do to plan for the unexpected?

No matter who you are or what stage of life you are at it’s never too late to get your finances in order and grow your wealth. We have outlined one key step below to assist you in doing just that. It’s simple, easily achieved and if followed means that you are taking your first steps in ensuring a brighter financial future for yourself and your family.

If you have a home loan, you should consider a home loan offset account and your income should be going into this account however frequently you’re paid.

Consider this basic situation:

- Home loan amount – $300,000

- Term – 30 years

- Interest rate – 4.1% per year

- Repayment frequency – monthly

- No offset account = zero interest saved, term remains at 30 years

ACTION: Link an offset account:

- Kick the offset account off with a $5,000 deposit from day one (and keep the average balance at $5,000)

- Deposit a monthly salary of $5,000 into the offset account

Result:

- Interest saved – $221,854

- Loan paid of – 17 years & 9 months earlier

That is a $221,854 saving – TAX FREE.

Read more about debt management

Assumptions

Timing assumptions

Loan repayments are assumed to be made at the end of each month or fortnight (depending on the repayment frequency you select). Loan repayments are assumed to occur immediately after the accrued loan interest has been charged to the loan. One year is assumed to contain exactly 26 fortnights or 12 months. This implicitly assumes that a year has 364 days rather than the actual 365 or 366.All months are assumed to be of equal length.

Loan interest rate

The loan interest rate you enter into the calculator is assumed to be the annual nominal rate of interest, compounded per the loan repayment frequency. For example, for a loan interest of 6.00% p.a. and monthly repayments, the calculator assumes the interest rate charged is (6.00% / 12) = 0.5% per month, compounded monthly. The loan interest rate you enter into the calculator is assumed to remain the applicable loan interest rate over the entire term of the loan.

Offset account

The average offset balance is assumed to not change over the selected repayment frequency period.

Loan repayments

The weekly and fortnightly loan repayment amounts are assumed to be a quarter and a half of the monthly repayment amount respectively. The loan repayment amount is calculated assuming a standard home loan where both interest and principal is repaid over the loan term.

Disclaimer

This calculator is provided by Rice Warner (ABN 35 003 186 883) and published by AMP Life Limited (ABN 84 079 300 379) AFSL 233 671 (AMP Life). The results provided by this calculator are indicative only, actual amounts may be higher or lower. They are based on the accuracy of the data entered into the calculators and a change in factors may vary the result. No representation is made as to your capacity to borrow money or to repay any loan. To help you consider the impact of interest rate changes we suggest exploring the impact of a rise in interest rates. The results do not constitute an offer to lend you money. Your financial situation and the suitability of a loan can only be assessed after a lender has made reasonable enquiries to ascertain these matters. Please be aware that your lender may also charge additional fees and charges. The calculator and the results provided are generic and do not take into account your personal circumstances. The calculator is a guide only and is not intended to be relied upon for the purposes of making a decision in relation to a credit or financial product. The user should obtain professional advice before making any financial decision. Other than as required by consumer protection law, under no circumstances will AMP Life and its related bodies corporate be liable for any loss and/or damage caused by a user’s reliance on information obtained by using this calculator.

If you think that your super will be sufficient to “fall back” on if all else fails in your retirement plan – this may not truly be the case. In point of fact the mean super balance for a person aged 55 – 65 is around $165,000(1) and in 2008 almost 70%(2) of the retiring population were resorting to Government Aged Pension. Clearly employer super isn’t sufficient for the current set of retirees.

One misconception is that forgetting about superannuation and concentrating on other investments ends up with enough in retirement.

We tend to find that those people who take their super seriously also succeed in the other areas of their wealth management.

Why is this, you may ask? Well it’s not because they’re amazing at choosing investments or know something others don’t, rather it’s because they become serious about the basics… Yes the basics of consistent savings, long term investment and the marvel of compounding!

There is also some great stuff we can do if you use a mortgage offset account. FIND OUT MORE

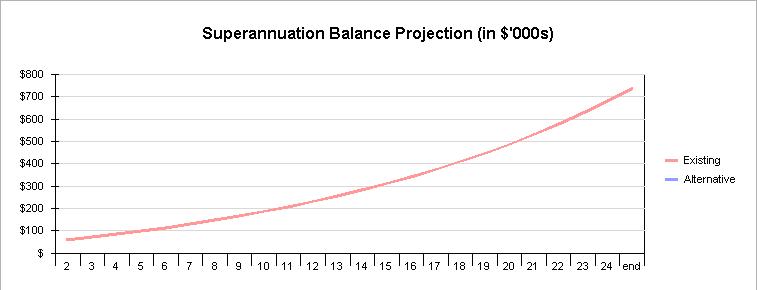

How much is enough?

To help you understand the basics, we’ll first show you ‘How much is enough?’ For a couple aged 35 years old looking to retire at age 60 on an income of $60,000 per annum, they’ll need to have superannuation savings of around $1.1 million dollars (3). Unfortunately for them the contributions from their employer won’t cut it, even at 12%. If that same couple has an annual income of $80,000 and $50,000 in superannuation already, they’re only going to reach a balance of around $800,000 (4), that’s $300,000 short of what they really need.

1. A little less in fees

2. A little extra savings

3. Putting them both together!

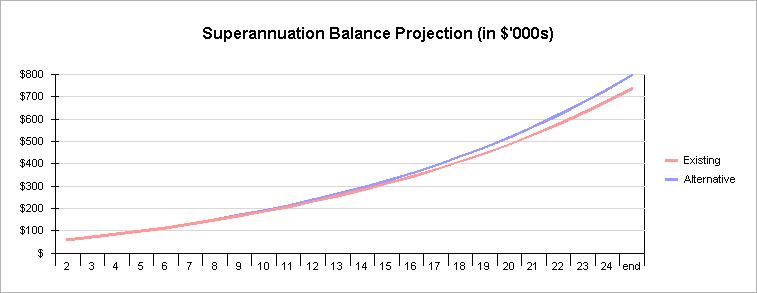

Strategy one – A little less fees in Superannuation

The power of compounding can work in both ways, in the same way that larger investment returns will increase your investment, so too will a reduction in investment fees. Look at it this way: would you rather have an investment returning 10% per annum and costing 4% in fees or an investment retuning 8% with only 1% in fees? We know which one we’d prefer.

In this strategy we look at the effect of reviewing the type of super fund you have and finding a lower cost alternative. Again using our same couple from earlier we get them to move their Super into a new fund with total fees half a percent (0.5%) cheaper per annum over the life of the investment without changing anything else.

Result: By the time they reach age 60 they would have a balance $866,524, that’s an extra $68,000, purely from saving only 0.5% in fees per annum. And this is not hard to achieve, if you find a good Superannuation Advisor they can often recommend a lower cost alternative, especially if you have multiple superannuation accounts already.

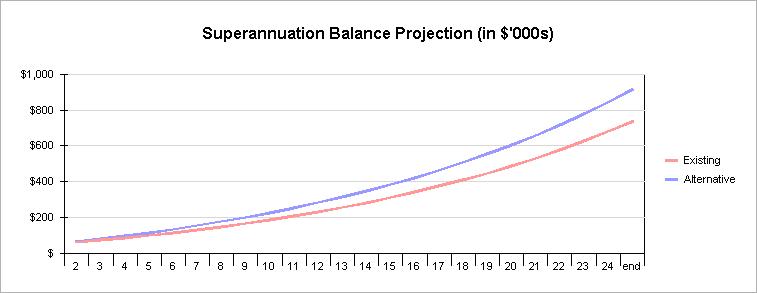

Strategy two – A little extra savings to Superannuation

Effective and consistent savings is arguably one of the most powerful habits of any successful investor. Take for example Warren Buffet, who made his first major investment at age 14 with $1,200 he saved doing a newspaper round, through adding more to his investment and then reinvesting the profits he now has a personal net worth of $47 Billion. “When you first make money, you may be tempted to spend it. Don’t. Instead, reinvest the profits”.

In this strategy we look at the effects of saving just a little extra via salary sacrifice. For a person earning $80,000 per annum an extra 5% per year is only $10.95 per day, probably less than you would spend on lunch! Using the same couple as in the last strategy they add an extra $10.95 per day to super without changing anything else.

Result: By the time they reach age 60 they would have a balance $988,000, that’s an extra $190,000!

Putting both strategies together!

Finally let’s see what happens when our couple puts strategy one and two together. An extra $4,000 per annum in salary sacrifice and a saving in fees of 0.5%.

Result: By the time they reach age 60 they would have a projected Super balance of $1.076 million. That’s an extra $278,000!!! Much closer to their goal of $60,000 per annum income in retirement.

Getting started on the basics

So there you have it, simply doing the basics consistently right will make a world of difference for your retirement planning and wealth creation and trust us; saving a little extra won’t break the bank, once you start you won’t even notice it. Applying this same set of principles across all your investments, not just superannuation then becomes easy and with that you will have even greater success.

If you are going to make one smart financial commitment this year it should be to speak to your Superannuation Advisor so that you too can make a start on these basics.

General Advice Warning: It is important for you to note that in preparing this article Cedar Wealth Financial Advisers have not taken into account any particular persons objectives, financial situation or needs. Investors should, before acting on this information, consider the appropriateness of this information having regard to their personal objectives, financial situation or needs. We recommend investors obtain financial advice specific to their situation before making any financial investment or insurance decision.

1. ABS 4102.0 – Australian Social Trends, March 2009 Pg 2.

2. Employment Arrangements, Retirement and Superannuation, Australia, April to July 2007 (Reissue)

(ABS cat. no. 6361.0).

3. This figure was derived using an annual income return of 5.5% p.a. net of fees and taxes.

4. For our projections we assumed a ‘Balanced’ total return of 8.5% p.a. net of taxes and fees and SCG

contributions of 12% p.a.